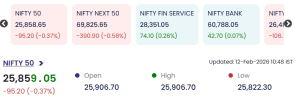

Indian equities traded under pressure on Thursday morning, with the benchmark Nifty 50 slipping to 25,859.05, down 95.20 points (-0.37%) as of 10:48 IST on 12 February 2026. The market’s weakness was largely driven by a sharp sell-off in frontline IT stocks, even as select financials and energy names offered partial support. Broader cues remained mixed: Nifty Next 50 underperformed, while Nifty Financial Services and Nifty Bank showed mild resilience.

Market Snapshot: Benchmarks Turn Cautious

-

Nifty 50: 25,859.05, down 0.37%

-

Day’s range: High 25,906.70 | Low 25,822.30

Day’s range: High 25,906.70 | Low 25,822.30 -

Nifty Next 50: Down 0.56%, indicating pressure in broader large-caps

-

Nifty Financial Services: Up 0.26%, reflecting selective buying in lenders and NBFCs

-

Nifty Bank: Up 0.07%, largely flat but supportive at the margin

Day’s range: High 25,906.70 | Low 25,822.30

Day’s range: High 25,906.70 | Low 25,822.30The index opened higher but failed to sustain momentum, slipping as selling intensified in technology heavyweights.

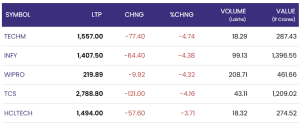

IT Stocks Lead the Decline

Technology counters were the clear laggards, dragging the headline index lower with steep intraday cuts:

-

Tech Mahindra fell 4.74%

-

Infosys slipped 4.38%

-

Wipro declined 4.32%

-

TCS shed 4.16%

-

HCL Technologies dropped 3.71%

Infosys slipped 4.38%

Infosys slipped 4.38%Heavy volumes in these names suggested broad-based profit-taking or risk-off positioning in the IT space, which remains sensitive to global growth cues and currency movements. The synchronized sell-off across tier-1 IT stocks amplified downside pressure on the Nifty despite stability elsewhere.

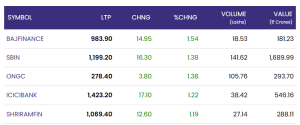

Financials and Energy Provide a Buffer

In contrast, select financial and energy stocks traded firm, helping limit the overall damage:

-

Bajaj Finance gained 1.54%

-

SBI advanced 1.38%

-

ICICI Bank rose 1.22%

-

Shriram Finance added 1.19%

-

ONGC climbed 1.38%

SBI advanced 1.38%

SBI advanced 1.38%Strength in lenders and NBFCs points to continued investor preference for domestically oriented, earnings-visibility sectors. ONGC’s uptick also provided sectoral support from the energy pack.

What’s Driving the Divergence?

The session highlighted a clear sectoral split—export-oriented IT stocks faced selling pressure, while financials remained relatively insulated. This divergence suggests investors are rotating toward sectors with stronger near-term domestic demand visibility and away from segments perceived to be more vulnerable to global macro uncertainty.

Conclusion: 12 February 2026

With the Nifty 50 easing below 25,900, the market tone remains cautious in the near term. The sharp IT sell-off underscores sector-specific risks, while steady gains in financials and energy indicate selective buying interest. Going ahead, index direction is likely to hinge on whether financials can continue to offset weakness in technology stocks, and on how global cues shape sentiment in export-heavy sectors.

For real time stock Updates, visit NSE website.