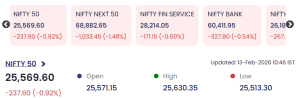

Indian equity markets opened the session on a weak footing on 13 February 2026, with the benchmark Nifty 50 slipping to 25,569.60, down 237.60 points (-0.92%) as of 10:46 IST. The sell-off was broad-based, with sharp losses in the Nifty Next 50, Nifty Financial Services, and Nifty Bank indices reflecting pressure across sectors. While a handful of frontline financial and consumption names managed to post modest gains, sustained selling in metals, IT, and energy stocks dragged the benchmark lower.

Market Snapshot: Broad-Based Weakness

-

Nifty 50: 25,569.60, down 0.92%

-

Day’s range: High 25,630.35 | Low 25,513.30

Day’s range: High 25,630.35 | Low 25,513.30 -

Nifty Next 50: Down 1.48%, signalling sharper pressure in the broader large-cap space

-

Nifty Financial Services: Down 0.60%

-

Nifty Bank: Down 0.54%

Day’s range: High 25,630.35 | Low 25,513.30

Day’s range: High 25,630.35 | Low 25,513.30The index opened near the day’s low and failed to stage a meaningful recovery, indicating cautious sentiment and continued risk-off positioning among investors.

Gainers: Financials and Select Cyclicals Show Resilience

Amid the broader sell-off, a few stocks managed to stay in the green, led primarily by financials and select consumption and auto names:

-

Bajaj Finance gained 1.34%, emerging as the top gainer in early trade

-

Apollo Hospitals rose 0.44%, indicating defensive buying in healthcare

-

Eicher Motors advanced 0.26%, supporting the auto pack

-

SBI added 0.25%

-

SBI Life edged up 0.17%

Eicher Motors advanced 0.26%, supporting the auto pack

Eicher Motors advanced 0.26%, supporting the auto packThe relative outperformance of these stocks suggests that investors are still selectively favouring quality financials and defensives amid heightened volatility.

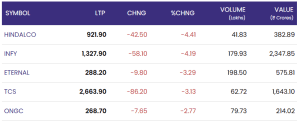

Losers: Metals, IT and Energy Stocks Drag the Index

Selling pressure was pronounced in metals, IT, and energy counters, which weighed heavily on the benchmark:

-

Hindalco fell 4.41%, leading the losers’ list

-

Infosys declined 4.19%, extending weakness in the IT space

-

Eternal (Zomato/Eternal brand) slipped 3.29%

-

TCS dropped 3.13%

-

ONGC eased 2.77%

Eternal (Zomato/Eternal brand) slipped 3.29%

Eternal (Zomato/Eternal brand) slipped 3.29%Heavy volumes in these names point to continued profit-taking and risk aversion, particularly in export-oriented IT stocks and cyclical sectors sensitive to global growth cues and commodity price movements.

Sectoral Trend: Pressure Across the Board, Selective Buying Continues

The sharp fall in the Nifty Next 50 underscores that the weakness is not limited to a few heavyweight stocks but is spread across the broader market. While financials also traded lower at the index level, selective buying in stocks like Bajaj Finance, SBI, and SBI Life helped cushion some of the downside. However, persistent selling in metals, IT, and energy stocks kept overall sentiment subdued.

Conclusion: 13 February 2026

With the Nifty 50 down nearly 1% at 25,569.60, market sentiment remains clearly risk-averse in the early trade on 13 February 2026. The combination of broad-based selling and sharp cuts in metals, IT, and energy stocks continues to pressure the indices, even as select financials and defensives offer limited support. In the near term, market direction is likely to hinge on whether broader market weakness stabilises and whether buying interest in quality large-caps can regain traction amid uncertain global and domestic cues.

For real time stock Updates, visit NSE website.