Mumbai, 09 February 2026 (14:16 IST) — Indian equities traded with a positive bias through the afternoon session on Monday, with the NIFTY 50 consolidating near record territory. Strength in banking, financials, and select industrial names kept the benchmarks in the green, even as selling pressure in IT, FMCG, and energy stocks capped the upside.

📊 Benchmarks Stay Firm, NIFTY Above 25,800

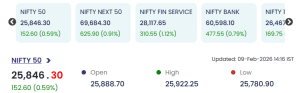

The NIFTY 50 was trading at 25,846.30, up 152.60 points (+0.59%), after opening at 25,888.70 and touching an intraday high of 25,922.25. The index saw a low of 25,780.90, indicating healthy intraday volatility but a clear bias towards consolidation at higher levels.

The NIFTY 50 was trading at 25,846.30, up 152.60 points (+0.59%), after opening at 25,888.70 and touching an intraday high of 25,922.25. The index saw a low of 25,780.90, indicating healthy intraday volatility but a clear bias towards consolidation at higher levels.

Broader indices also reflected strength, with NIFTY Next 50 up 0.91%, NIFTY Financial Services gaining 1.12%, and NIFTY Bank rising 0.79%, underlining continued investor preference for financial and cyclical stocks.

🏦 Financials and Cyclicals Lead the Market

Buying interest remained concentrated in heavyweight financial and industrial names, pushing several stocks to the top of the gainers’ list:

-

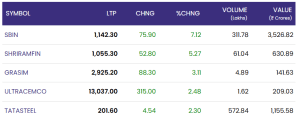

State Bank of India (SBI) surged 7.12% to ₹1,142.30, with strong turnover of over 31 lakh shares and value exceeding ₹3,500 crore, highlighting sustained institutional interest.

-

Shriram Finance jumped 5.27% to ₹1,055.30, supported by healthy volumes, as NBFC stocks continued to attract momentum traders.

-

Grasim Industries advanced 3.11% to ₹2,925.20, reinforcing the positive tone in diversified industrial plays.

Grasim Industries advanced 3.11% to ₹2,925.20, reinforcing the positive tone in diversified industrial plays. -

UltraTech Cement gained 2.48% to ₹13,037, reflecting steady demand in core infrastructure and construction-linked stocks.

-

Tata Steel added 2.30% to ₹201.60, with heavy volumes of over 570 lakh shares, indicating strong participation in the metals space.

Grasim Industries advanced 3.11% to ₹2,925.20, reinforcing the positive tone in diversified industrial plays.

Grasim Industries advanced 3.11% to ₹2,925.20, reinforcing the positive tone in diversified industrial plays.The rally in these names helped offset weakness in select large-cap defensives and technology stocks.

📉 IT, FMCG and Energy Stocks Face Selling Pressure

Despite the broader market’s positive bias, several frontline stocks traded in the red as investors booked profits at higher levels:

-

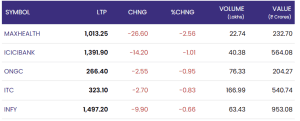

Max Healthcare declined 2.56% to ₹1,013.25, emerging as one of the top laggards of the session.

-

ICICI Bank slipped 1.01% to ₹1,391.90, showing mild consolidation after recent gains.

-

ONGC eased 0.95% to ₹266.40, tracking softer cues in the energy space.

-

ITC fell 0.83% to ₹323.10, while Infosys lost 0.66% to ₹1,497.20, reflecting continued rotation away from defensives and IT counters.

ONGC eased 0.95% to ₹266.40, tracking softer cues in the energy space.

ONGC eased 0.95% to ₹266.40, tracking softer cues in the energy space.This mixed sectoral performance points to a market that is selectively rewarding growth and cyclical exposure while trimming positions in relatively defensive segments.

🧠 Market View: Consolidation with a Positive Bias

Market participants noted that the indices are consolidating at elevated levels after the recent rally, with stock-specific action dominating intraday moves. The strong showing by banks and finance stocks suggests confidence in the earnings outlook and balance sheet strength of lenders and NBFCs. At the same time, profit-taking in IT and FMCG indicates a tactical shift towards higher-beta sectors.

📌 Conclusion: 9 February 2026

The Indian equity market on Monday showcased selective strength, with the NIFTY 50 holding above 25,800 and financials, metals, and industrials driving gains. While pockets of weakness in IT, FMCG, and energy kept the indices from a sharper rise, the overall tone remains constructive. Going forward, investors are likely to watch global cues, interest rate expectations, and upcoming macro data for the next directional trigger.

For real time stock Updates, visit NSE website.