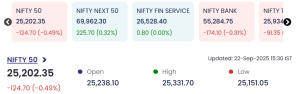

Mumbai: On September 22, 2025, benchmark indices in India witnessed a broad decline led by heavy selling in information technology shares, with Nifty 50 closing at 25,202.35, down 124.70 points (-0.49%). Market sentiment wavered on the back of global uncertainty and the adverse impact of new US H-1B visa fee rules, hitting IT stocks and influencing key sectoral indices.

Key Index Performances

Nifty 50 traded in the range of 25,151.05 (low) to 25,331.70 (high), opening at 25,238.10 before closing at 25,202.35, marking a notable pullback from last week’s highs. The Nifty Next 50 showed resilience, gaining 225.70 points (+0.32%) at 69,962.30, while Nifty Fin Service was flat (+0.00%). Nifty Bank slipped 174.10 points (-0.31%) to finish at 55,284.75, underscoring subdued momentum across the banking segment.

Nifty 50 traded in the range of 25,151.05 (low) to 25,331.70 (high), opening at 25,238.10 before closing at 25,202.35, marking a notable pullback from last week’s highs. The Nifty Next 50 showed resilience, gaining 225.70 points (+0.32%) at 69,962.30, while Nifty Fin Service was flat (+0.00%). Nifty Bank slipped 174.10 points (-0.31%) to finish at 55,284.75, underscoring subdued momentum across the banking segment.

Sector and Stock Movers

-

The IT sector was hardest hit, with the Nifty IT index losing 3%, as global cues and new US visa fees prompted profit-taking in marquee stocks like TCS, Infosys, HCL Tech, and Wipro.

The IT sector was hardest hit, with the Nifty IT index losing 3%, as global cues and new US visa fees prompted profit-taking in marquee stocks like TCS, Infosys, HCL Tech, and Wipro. -

Pharma and FMCG indices also lagged, with declines of 1.4% and 0.5%, respectively, while the Nifty Metal index stood out with a modest gain of 0.5%.

-

Market breadth remained negative with Nifty MidCap (-0.67%) and SmallCap (-1.17%) indices in the red.

The IT sector was hardest hit, with the Nifty IT index losing 3%, as global cues and new US visa fees prompted profit-taking in marquee stocks like TCS, Infosys, HCL Tech, and Wipro.

The IT sector was hardest hit, with the Nifty IT index losing 3%, as global cues and new US visa fees prompted profit-taking in marquee stocks like TCS, Infosys, HCL Tech, and Wipro.Technical Overview and Market Sentiment

Short-term technical indicators suggest support for Nifty 50 near 25,050; a breach could extend the correction towards 24,800. Resistance is pegged at 25,250, a move above which could trigger renewed buying. Analysts note that recent corrections follow a sharp 1,000-point rally in the broader index—often viewed as a healthy pause in ongoing market momentum.

Top Gainers and Losers

-

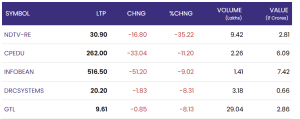

Significant losers included Tech Mahindra, TCS, Infosys, Wipro, HCL Tech, and Tata Motors, all recording declines between 1% and 3%.

-

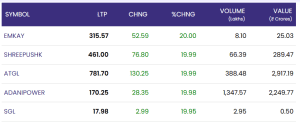

On the other hand, Adani Enterprises, Eternal, Bajaj Finance, Adani Ports, and Ultratech Cement outperformed, with gains as high as 4%.

Significant losers included Tech Mahindra, TCS, Infosys, Wipro, HCL Tech, and Tata Motors, all recording declines between 1% and 3%.

Significant losers included Tech Mahindra, TCS, Infosys, Wipro, HCL Tech, and Tata Motors, all recording declines between 1% and 3%.Market Volatility and Outlook

The India VIX volatility index jumped 5.8%, indicating heightened market nervousness amid the global policy action and sector rotation. While the index pullback signals near-term caution, investors remain optimistic about underlying economic strength, drawing confidence from a recent foreign portfolio investor (FPI) inflow.

Conclusion: September 22, 2025

The trading session on September 22, 2025, highlighted risk-off sentiment as IT sector headwinds dragged benchmark indices lower. However, underlying support levels remain intact, and the correction may provide opportunities for accumulation in fundamentally strong sectors.

For real time stock Updates, visit NSE website.