Indian equity markets witnessed a sharp reversal in the latter half of the session on 1 February 2026, with benchmarks closing deep in the red amid broad-based selling pressure. Weak sentiment across banking, financial services, energy, and PSU stocks weighed heavily on indices, overshadowing selective buying in IT and pharmaceutical counters.

Benchmark Performance: Nifty Breaks Key Support

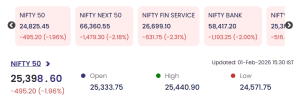

The Nifty 50 closed at 25,398.60, plunging 495.20 points (-1.96%). The index opened at 25,333.75, touched an intraday high of 25,440.90, but slipped to a low of 24,571.75, reflecting aggressive selling during the latter half of the session.

Other key indices mirrored the weakness:

-

Nifty Bank dropped 2.00% to 58,417.20, emerging as one of the worst-performing sectors.

Nifty Bank dropped 2.00% to 58,417.20, emerging as one of the worst-performing sectors. -

Nifty Financial Services declined 2.31% to 26,699.10, indicating sustained pressure on lenders and NBFCs.

-

Nifty Next 50 shed 2.18%, signaling risk aversion across broader markets.

Nifty Bank dropped 2.00% to 58,417.20, emerging as one of the worst-performing sectors.

Nifty Bank dropped 2.00% to 58,417.20, emerging as one of the worst-performing sectors.

Market Breadth: Declines Overwhelm Advances

Market breadth remained decisively negative, with a majority of index constituents ending lower. Heavy volumes in declining stocks suggested institutional selling rather than retail profit-booking, pointing to a cautious near-term outlook.

Top Gainers: IT and Pharma Offer Limited Support

Despite the overall sell-off, select defensive and export-oriented stocks provided some relief:

-

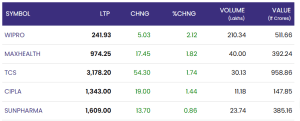

Wipro gained 2.12% to ₹241.93, supported by strong volumes, as IT stocks attracted selective buying.

-

TCS rose 1.74% to ₹3,178.20, offering stability to the technology pack.

-

Max Healthcare advanced 1.82% to ₹974.25, continuing its recent positive momentum.

-

Cipla climbed 1.44% to ₹1,343.00, while

-

Sun Pharma added 0.86% to ₹1,609.00, reinforcing the defensive appeal of pharmaceuticals.

TCS rose 1.74% to ₹3,178.20, offering stability to the technology pack.

TCS rose 1.74% to ₹3,178.20, offering stability to the technology pack.Top Losers: Banks, Metals, and PSUs Bear the Brunt

Selling pressure was most pronounced in financials, metals, and PSU stocks:

-

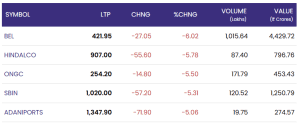

BEL slumped 6.02% to ₹421.95, recording the steepest decline among key names amid heavy volumes.

-

Hindalco fell 5.78% to ₹907.00, tracking weakness in metal prices.

-

ONGC declined 5.50% to ₹254.20, reflecting pressure in the energy space.

-

SBIN dropped 5.31% to ₹1,020.00, weighing significantly on the Bank Nifty.

-

Adani Ports slid 5.06% to ₹1,347.90, adding to the drag on frontline indices.

ONGC declined 5.50% to ₹254.20, reflecting pressure in the energy space.

ONGC declined 5.50% to ₹254.20, reflecting pressure in the energy space.What Drove the Market Downturn

The sharp fall highlights heightened risk aversion, with investors trimming exposure to cyclicals and PSU-heavy segments. Weakness in banking and energy stocks amplified downside momentum, while limited support from defensives was insufficient to arrest the decline.

Conclusion: 1 February 2026

The session marked a decisive bearish close for Indian equities, with the Nifty 50 breaking below key psychological levels amid broad-based selling. While IT and pharma stocks offered pockets of resilience, sustained pressure on banks, metals, and PSUs kept sentiment fragile. Near-term market direction is likely to remain volatile, with investors closely monitoring sectoral cues and institutional flows.

For real time stock Updates, visit NSE website.