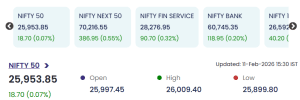

Indian equity markets closed the session on February 11, 2026, on a muted note, with the NIFTY 50 settling at 25,953.85, up a marginal 0.07%. The benchmark spent the day in a tight range, as strong gains in healthcare and banking stocks were offset by sharp declines in IT majors. The session reflected continued sector rotation, with investors preferring defensives and select cyclicals while trimming exposure to technology stocks.

Benchmarks: Narrow-Range Close Near 26,000

The NIFTY 50 opened at 25,997.45 and traded between a high of 26,009.40 and a low of 25,899.80, before closing just below the 25,960 mark. Broader indices showed relatively better momentum:

-

NIFTY Next 50 climbed 0.55% to 70,216.55, signaling stronger participation beyond the frontline stocks.

-

NIFTY Fin Service rose 0.32% to 28,276.95, supported by buying in select financial heavyweights.

NIFTY Fin Service rose 0.32% to 28,276.95, supported by buying in select financial heavyweights. -

NIFTY Bank added 0.20% to 60,745.35, aided by strong performance in PSU banks.

NIFTY Fin Service rose 0.32% to 28,276.95, supported by buying in select financial heavyweights.

NIFTY Fin Service rose 0.32% to 28,276.95, supported by buying in select financial heavyweights.Despite these gains, weakness in IT heavyweights capped the upside for the headline index.

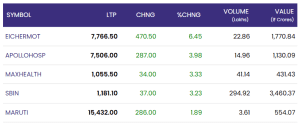

Gainers: Healthcare and Banks Lead, Autos Support

Stocks from the healthcare and banking space dominated the gainers’ list, supported by robust volumes:

-

Eicher Motors surged 6.45% to ₹7,766.50, emerging as the top gainer of the session on sustained buying interest.

-

Apollo Hospitals advanced 3.98% to ₹7,506, extending strength in hospital stocks.

-

Max Healthcare rose 3.33% to ₹1,055.50, reinforcing the positive sentiment in the healthcare sector.

-

State Bank of India (SBI) climbed 3.23% to ₹1,181.10, providing a strong boost to the banking index with heavy volumes.

-

Maruti Suzuki gained 1.89% to ₹15,432, adding support from the auto pack.

Max Healthcare rose 3.33% to ₹1,055.50, reinforcing the positive sentiment in the healthcare sector.

Max Healthcare rose 3.33% to ₹1,055.50, reinforcing the positive sentiment in the healthcare sector.The rally in these names highlighted investor preference for large, liquid stocks in defensive and financial segments.

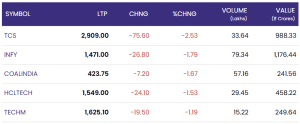

Losers: IT Majors Drag the Index: February 11, 2026

Technology stocks witnessed sharp selling pressure, emerging as the biggest drag on the market:

-

TCS fell 2.53% to ₹2,909, leading the losers’ pack amid heavy volumes.

-

Infosys slipped 1.79% to ₹1,471, extending weakness across the IT sector.

-

Coal India declined 1.67% to ₹423.75, reflecting softness in energy stocks.

-

HCL Technologies dropped 1.53% to ₹1,549, while Tech Mahindra lost 1.19% to ₹1,625.10.

Coal India declined 1.67% to ₹423.75, reflecting softness in energy stocks.

Coal India declined 1.67% to ₹423.75, reflecting softness in energy stocks.The broad-based sell-off in IT counters outweighed gains in healthcare and banks, keeping the benchmark largely flat.

Market View: Sector Rotation Keeps Indices Range-Bound

The day’s trade underlined the ongoing sector rotation theme in the market. While money flowed into healthcare, PSU banks and select auto stocks, persistent selling in IT majors prevented any meaningful breakout above the 26,000 mark. The narrow trading range suggests that investors are staying cautious at elevated levels, awaiting fresh cues to take directional positions.

Conclusion

The Indian equity market ended the session with marginal gains, as the NIFTY 50 closed near 25,954. Strong performances from healthcare and banking stocks were neutralized by sharp declines in IT majors. Going forward, market direction is likely to remain driven by sectoral shifts and stock-specific developments rather than broad-based momentum.

For real time stock Updates, visit NSE website.