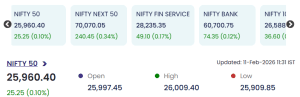

Indian equity markets traded with a cautious tone in the late morning session on February 11, 2026, with the NIFTY 50 hovering just below the 26,000 mark. The benchmark was marginally higher at 25,960.40, up 0.10%, as gains in pharma, banking and select auto names were offset by weakness in IT, metals and energy stocks. The session reflected a classic case of consolidation at elevated levels, with stock-specific action dominating the tape.

Benchmarks Show Mild Gains

The NIFTY 50 opened at 25,997.45 and moved in a narrow range, hitting a session high of 26,009.40 and a low of 25,909.85. Other key indices showed a slightly stronger tone:

-

NIFTY Next 50 rose 0.34% to 70,070.05, indicating better participation in the broader market.

-

NIFTY Fin Service gained 0.17% to 28,235.35, supported by select financial heavyweights.

NIFTY Fin Service gained 0.17% to 28,235.35, supported by select financial heavyweights. -

NIFTY Bank edged up 0.12% to 60,700.75, reflecting a steady but cautious banking space.

NIFTY Fin Service gained 0.17% to 28,235.35, supported by select financial heavyweights.

NIFTY Fin Service gained 0.17% to 28,235.35, supported by select financial heavyweights.Overall, the market remained range-bound, with investors unwilling to take aggressive bets near record levels.

Gainers: Pharma, Banks and Autos in Focus

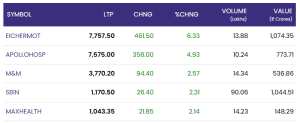

Buying interest was visible in select large-cap and high-volume counters, led by pharma and banking names:

-

Eicher Motors jumped 6.33% to ₹7,757.50, emerging as the top gainer of the session on strong buying interest.

-

Apollo Hospitals rose 4.93% to ₹7,575, reflecting strength in healthcare stocks.

-

Mahindra & Mahindra added 2.57% to ₹3,770.20, extending momentum in the auto pack.

-

State Bank of India (SBI) advanced 2.31% to ₹1,170.50, providing support to the banking index.

-

Max Healthcare gained 2.14% to ₹1,043.35, continuing the positive trend in hospital stocks.

Mahindra & Mahindra added 2.57% to ₹3,770.20, extending momentum in the auto pack.

Mahindra & Mahindra added 2.57% to ₹3,770.20, extending momentum in the auto pack.The performance of these stocks highlighted a preference for defensives like healthcare alongside select cyclicals such as autos and banks.

Losers: IT, Metals and Energy See Mild Selling: February 11, 2026

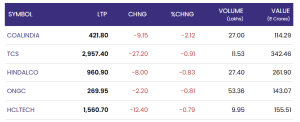

On the downside, profit-taking was visible in a few heavyweight sectors, limiting the benchmark’s upside:

-

Coal India declined 2.12% to ₹421.80, leading the losers’ pack amid weakness in energy stocks.

-

TCS fell 0.91% to ₹2,957.40, reflecting continued pressure on IT majors.

-

Hindalco slipped 0.83% to ₹960.90, as metal stocks cooled off after recent gains.

-

ONGC eased 0.81% to ₹269.95, while HCL Technologies lost 0.79% to ₹1,560.70.

Hindalco slipped 0.83% to ₹960.90, as metal stocks cooled off after recent gains.

Hindalco slipped 0.83% to ₹960.90, as metal stocks cooled off after recent gains.The softness in IT, metals and energy stocks offset the gains in pharma and banking counters.

Market View: Consolidation Continues Near Record Levels

With the NIFTY 50 trading just below 26,000, the broader market appears to be in a consolidation phase after the recent rally. Sector rotation remains the key theme, with investors selectively accumulating pharma, healthcare and banking stocks while trimming exposure in IT, metals and energy. The narrow trading range suggests that participants are waiting for fresh triggers before committing to a directional move.

Conclusion

The Indian equity market remained largely flat with a positive bias, as the NIFTY 50 held near 25,960. Strength in pharma, healthcare, banks and select auto stocks provided support, but weakness in IT, metals and energy capped the upside. In the near term, markets are likely to stay range-bound, driven more by stock-specific developments and sectoral rotation than by broad-based momentum.

For real time stock Updates, visit NSE website.