Indian equities continued to consolidate in the early afternoon session on February 11, 2026, with the NIFTY 50 trading marginally higher at 25,957.30, up 0.09%. The index remained confined to a narrow band, as strong buying in healthcare and banking stocks was offset by persistent weakness in IT, energy and select FMCG names. The overall tone suggested cautious optimism, with investors preferring stock-specific bets over broad-based risk-taking.

Benchmarks Hold Steady at Elevated Levels

The NIFTY 50 opened at 25,997.45 and moved within a tight range, touching a session high of 26,009.40 and a low of 25,899.80. Other indices showed relatively better momentum:

-

NIFTY Next 50 gained 0.42% to 70,124.95, indicating improved participation in the broader market.

-

NIFTY Fin Service rose 0.25% to 28,256.00, supported by select financial heavyweights.

NIFTY Fin Service rose 0.25% to 28,256.00, supported by select financial heavyweights. -

NIFTY Bank advanced 0.16% to 60,721.90, aided by strength in large PSU and private banks.

NIFTY Fin Service rose 0.25% to 28,256.00, supported by select financial heavyweights.

NIFTY Fin Service rose 0.25% to 28,256.00, supported by select financial heavyweights.Despite these gains, the headline index struggled to break decisively above the 26,000 mark.

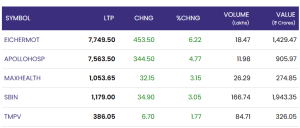

Gainers: Healthcare and Banking Stocks in the Lead

Healthcare and banking names dominated the gainers’ list, backed by strong volumes and sustained buying interest:

-

Eicher Motors surged 6.22% to ₹7,749.50, retaining its position as the top gainer and reflecting strong momentum in premium auto stocks.

-

Apollo Hospitals climbed 4.77% to ₹7,563.50, extending the rally in healthcare counters.

-

Max Healthcare added 3.15% to ₹1,053.65, highlighting continued investor interest in hospital stocks.

-

State Bank of India (SBI) rose 3.05% to ₹1,179.00, providing a solid boost to the banking index.

-

Tata Motors PV (TMPV) gained 1.77% to ₹386.05, indicating selective buying in auto-related names.

Max Healthcare added 3.15% to ₹1,053.65, highlighting continued investor interest in hospital stocks.

Max Healthcare added 3.15% to ₹1,053.65, highlighting continued investor interest in hospital stocks.The strength in these stocks underscored a defensive-cum-cyclical mix, with investors favouring healthcare and large banks.

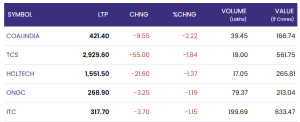

Losers: IT, Energy and FMCG See Continued Pressure: February 11, 2026

On the downside, selling pressure persisted in IT, energy and select consumer names, limiting the benchmark’s upside:

-

Coal India fell 2.22% to ₹421.40, leading the losers amid weakness in energy stocks.

-

TCS slipped 1.84% to ₹2,929.60, extending the decline in IT majors.

-

HCL Technologies dropped 1.37% to ₹1,551.50, keeping the IT pack under pressure.

-

ONGC eased 1.19% to ₹268.90, reflecting subdued sentiment in oil and gas counters.

-

ITC declined 1.15% to ₹317.70, adding to the drag from FMCG heavyweights.

HCL Technologies dropped 1.37% to ₹1,551.50, keeping the IT pack under pressure.

HCL Technologies dropped 1.37% to ₹1,551.50, keeping the IT pack under pressure.The weakness in these large-cap stocks continued to cap any meaningful upside in the broader indices.

Market View: Sector Rotation Dominates, Breakout Elusive

The ongoing session reinforced the theme of sector rotation, with money flowing into healthcare and banking stocks while moving out of IT, energy and FMCG. The NIFTY 50’s inability to sustain above 26,000 suggests that investors are adopting a cautious stance near record levels, awaiting fresh cues before committing to a decisive directional move.

Conclusion

The Indian equity market remained in a consolidation phase, with the NIFTY 50 hovering near 25,957. Strong gains in healthcare and banking stocks offered support, but continued weakness in IT, energy and FMCG names kept the index range-bound. In the near term, markets are likely to stay driven by stock-specific developments and sectoral shifts rather than broad-based momentum.

For real time stock Updates, visit NSE website.