Indian equity markets closed in the red on Wednesday, January 21, 2026 as sustained selling in banking and financial stocks outweighed gains in select metal, healthcare and aviation counters. Despite touching fresh intraday highs, the Nifty 50 failed to hold momentum in the second half of the session, reflecting cautious investor sentiment and sectoral rotation.

Nifty 50 Closes Lower After Volatile Session

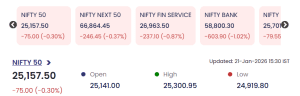

As of 15:30 IST on 21 January 2026, the Nifty 50 settled at 25,157.50, down 75 points (-0.30%).

-

Open: 25,141.00

-

Day’s High: 25,300.95

Day’s High: 25,300.95 -

Day’s Low: 24,919.80

Day’s High: 25,300.95

Day’s High: 25,300.95The index witnessed sharp intraday swings, briefly crossing the 25,300 mark before profit booking emerged. The inability to sustain higher levels suggests market participants remain selective and risk-averse at elevated valuations.

Broader Indices Also End in Red

Weakness was visible across key indices, indicating broad-based selling pressure:

-

Nifty Next 50: 66,864.45 (-0.37%)

-

Nifty Financial Services: 26,963.50 (-0.87%)

-

Nifty Bank: 58,800.30 (-1.02%)

The sharp decline in banking indices was the key drag on overall market performance.

Top Gainers: Eternal Leads, Metals and Healthcare Support

Buying interest remained in selective pockets of the market:

-

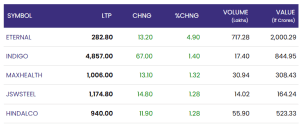

Eternal: ₹282.80, +4.90%

-

IndiGo (INDIGO): ₹4,857.00, +1.40%

-

Max Healthcare (MAXHEALTH): ₹1,006.00, +1.32%

-

JSW Steel (JSWSTEEL): ₹1,174.80, +1.28%

-

Hindalco: ₹940.00, +1.28%

Max Healthcare (MAXHEALTH): ₹1,006.00, +1.32%

Max Healthcare (MAXHEALTH): ₹1,006.00, +1.32%Strong volumes in Eternal highlighted continued investor interest, while gains in JSW Steel and Hindalco pointed to resilience in metal stocks. Healthcare and aviation counters also provided limited support to the broader market.

Top Losers: Banks and Consumer Stocks Face Heavy Selling

Losses were dominated by financial and consumption-oriented stocks:

-

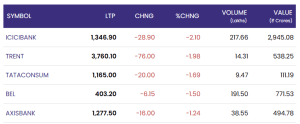

ICICI Bank: ₹1,346.90, -2.10%

-

Trent: ₹3,760.10, -1.98%

-

Tata Consumer Products: ₹1,165.00, -1.69%

-

BEL: ₹403.20, -1.50%

-

Axis Bank: ₹1,277.50, -1.24%

Tata Consumer Products: ₹1,165.00, -1.69%

Tata Consumer Products: ₹1,165.00, -1.69%The sharp decline in heavyweight lenders such as ICICI Bank and Axis Bank exerted significant pressure on the Nifty Bank, reinforcing the cautious tone in financials.

Market View: Sectoral Rotation, Not Panic Selling

The session reflected healthy sectoral rotation rather than aggressive risk-off sentiment. Investors appeared to book profits in banking and consumer stocks while reallocating selectively into metals, healthcare and high-momentum counters. Technically, the 24,900–25,000 zone continues to act as a strong support, while the 25,300–25,350 band remains a stiff resistance.

Conclusion: January 21, 2026

The market closed with modest losses but continues to show resilience through selective buying. While financial stocks remain under pressure, strength in metals, healthcare and specific momentum names suggests that investors are still deploying capital cautiously. Near-term direction will likely depend on institutional flows, earnings developments and global market cues.

For real time stock Updates, visit NSE website.